- While device volumes are shrinking, revenue is climbing as vendors push price increases through the channel faster than demand is cooling.

- Vendors are bracing for further price hikes into 2027, and channels are already flagging concern about elevated inventory at these higher price points.

Worldwide PC shipments fell 4.9 per cent year over year in the second quarter of 2026, dropping to 68.2 million units and marking the first contraction after nine consecutive quarters of growth, according to the latest data from IDC.

The reversal was driven primarily by a persistent and deepening memory chip shortage that has forced vendors to pull inventory forward as aggressively as possible — a tactic that IDC analysts now believe has largely run its course.

The memory crunch is not happening in isolation. AI data centers are projected to consume as much as 70 per cent of all memory chips produced in 2026, diverting supply away from the PC and consumer electronics segments and placing extraordinary strain on the entire semiconductor supply chain.

High-bandwidth memory (HBM), which is critical to AI accelerators, now accounts for roughly 23 per cent of total DRAM wafer output, creating what industry observers describe as a zero-sum contest between AI infrastructure and consumer devices.

Beyond memory, other components — including storage, power management ICs, and networking silicon — along with persistent geopolitical headwinds, have continued to weigh on the market.

The unit-revenue disconnect

Perhaps the most telling indicator of the market’s unusual state is the widening gap between unit shipments and dollar revenue. While device volumes are shrinking, revenue is climbing as vendors push price increases through the channel faster than demand is cooling.

“The real story here is the disconnect between units and dollars: shipments are falling, but revenue is climbing because vendors are pushing through price increases faster than demand is dropping,” said Jitesh Ubrani, research director for consumer devices at IDC.

He added a stark outlook for the remainder of the year: “Given worsening macro conditions and a memory shortage that isn’t expected to ease until early 2028, we don’t expect another round of inventory pull-forward, which points to a sharp slowdown in growth rates in the second half of 2026. Vendors are bracing for further price hikes into 2027, and channels are already flagging concern about elevated inventory at these higher price points.”

This dynamic is already visible in price trends. Global RAM prices are projected to spike by roughly 30 per cent in 2026 alone, and memory chips — which typically account for 15–18 per cent of a PC’s bill of materials — are exerting disproportionate pressure on manufacturer margins and end-consumer pricing.

IDC’s full-year forecast now calls for an 11.3 per cent decline in annual PC shipments, with an even sharper drop of approximately 20 per cent anticipated in the fourth quarter.

Two underlying trends

Beyond the headline numbers, two structural shifts are reshaping the competitive landscape.

The upgrade cycle under threat. Sustained cost pressure from the memory shortage risks cooling the broader PC refresh cycle just as interest in on-device AI processing is accelerating. Enterprises and consumers alike are being pulled in opposite directions: on-device AI workloads promise lower latency, better privacy, and insulation from rising cloud compute costs, yet the hardware capable of running those workloads is becoming significantly more expensive.

Entry-level AI-capable laptops have jumped from roughly $900–$1,200 to $1,400–$1,700, while power-user machines have climbed from $1,800–$2,200 to $2,800–$3,500 — increases of 50–75 per cent across both tiers.

AI Advanced PC penetration is still expected to reach roughly 59 per cent of global shipments in 2026, up from approximately 39 per cent in 2025, but the enterprise adoption curve is showing signs of deceleration after the Windows 10 end-of-support surge. A meaningful second wave of enterprise AI PC adoption now looks more likely to materialize in 2027.

Vendor consolidation accelerates. The memory shortage is proving to be a powerful forcing function for market concentration. Top-tier brands — Lenovo, HP, Dell, and Apple — are leveraging their scale across adjacent business lines, including smartphones, servers, and cloud infrastructure, to lock in preferential memory supply and squeeze out smaller competitors.

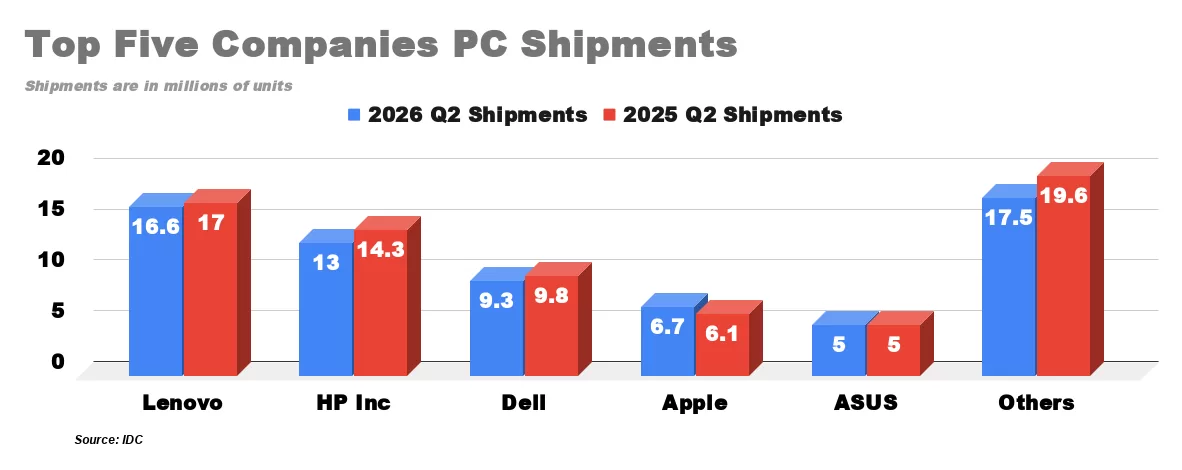

In Q2 2026, Lenovo held the top spot with 24.4 per cent market share despite a 2.1 per cent year-over-year shipment decline; HP followed at 19.1 per cent, with Dell at 13.6 per cent. Apple was the standout exception among major vendors, posting significant shipment growth driven by the March 2026 launch of the MacBook Neo, its most affordable laptop ever at \$599. The device sold out through April and has helped the company climb to fourth place globally with approximately 10.3 million units and a 14.8 per cent share.

“As market conditions continue to worsen, the importance of supply chain management and capabilities are increasingly important. The largest vendors, with their buying power and long-standing supplier ties, are best positioned to take share from smaller rivals,” said Jean Philippe Bouchard, vice president for consumer devices at IDC.

“Apple’s share gain coincided with its latest product launch, the MacBook Neo, and while the company did raise prices in line with the broader market, it still remains well positioned against rivals facing the same cost pressures.”

The outlook through the remainder of 2026 and into 2027 is cautious at best. The memory shortage, rooted in the structural imbalance between surging AI data center demand and finite semiconductor fabrication capacity, is not expected to ease until early 2028.

Synopsys CEO Sassine Ghazi reinforced this timeline in early 2026, stating publicly that price rises and supply constraints are likely to persist through 2027.

For PC vendors, this means navigating a prolonged period in which volume growth is off the table and pricing strategy becomes the primary lever for protecting margins. For buyers — whether enterprise IT departments or individual consumers — it means accepting that the era of steadily declining PC prices has, at least for now, come to an end.

The channel, meanwhile, is caught in the middle: inventories are elevated at price points that may prove difficult to sustain if macroeconomic conditions deteriorate further.

You must be logged in to post a comment.